how to get out of negative equity car finance

Finding yourself in a situation where your car is worth less than the outstanding balance on your loan can be a source of significant financial stress. This common predicament, known as negative equity or being “upside down” on your car loan, affects many vehicle owners, often due to rapid depreciation and lengthy financing terms. While it might seem like an inescapable trap, there are several practical strategies you can employ to address and ultimately resolve negative equity. Understanding these options is the first crucial step towards regaining control of your automotive finances and avoiding future complications.

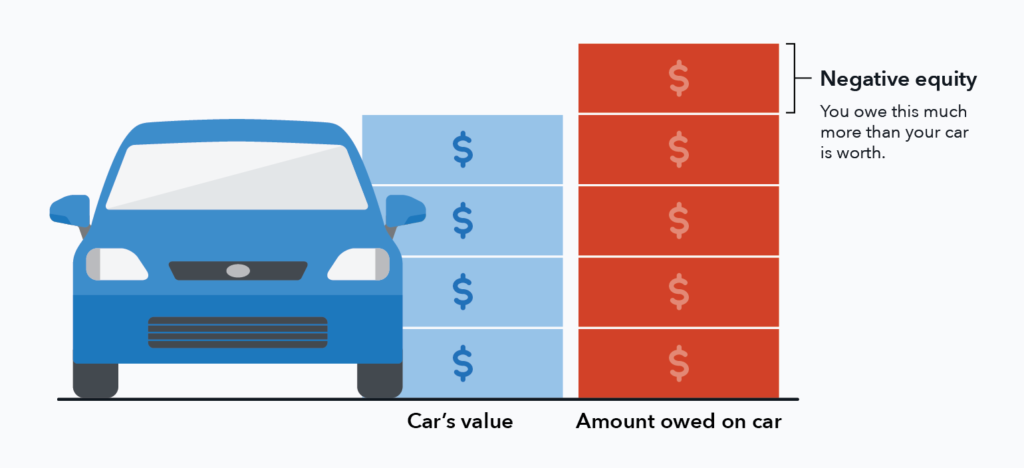

Understanding Negative Equity in Your Car Loan

Negative equity occurs when the market value of your vehicle falls below the amount you still owe on your car loan. This imbalance is primarily driven by the rapid depreciation of new cars; vehicles typically lose a significant portion of their value the moment they are driven off the lot. Other contributing factors include making a small down payment, financing for an extended period, or rolling previous negative equity into a new loan. Recognizing these elements helps illuminate why you might be in this challenging financial position.

Effective Strategies to Overcome Negative Car Equity

Addressing negative equity requires a clear understanding of your current financial standing and the potential paths forward. Each strategy comes with its own set of advantages and considerations, making it essential to evaluate which approach best suits your personal circumstances and financial goals.

Selling Your Car with Negative Equity

Selling your car independently can sometimes yield a better price than a trade-in, but it presents a unique challenge when negative equity is involved. You are still responsible for paying off the full loan balance, even if the sale price doesn’t cover it entirely. This means you would need to cover the difference out of pocket, often by using savings or taking out a personal loan. It’s a direct route to clearing the debt, provided you have the funds to bridge the gap.

Trading In a Vehicle with Negative Equity

Many people opt to trade in their car, even with negative equity, when purchasing a new one. The most common method is to roll the outstanding negative balance into the new car loan. While this can seem like an easy solution, it increases your new loan amount, leading to higher monthly payments and potentially a longer loan term. Alternatively, you could pay the difference between your car’s trade-in value and the loan balance at the time of trade-in, effectively starting your new loan on a clean slate.

Paying Down Your Car Loan Faster

Accelerating your loan payments is a proactive way to reduce negative equity over time. By reducing the principal balance more quickly, you can outpace the car’s depreciation. This strategy requires consistent effort and discipline but offers a direct path to positive equity. Here are a few ways to achieve this:

- Make extra payments whenever possible, even small amounts.

- Round up your monthly payment to the nearest whole number.

- Apply any unexpected windfalls, like tax refunds or bonuses, directly to the principal.

- Consider making bi-weekly payments, which can result in an extra payment per year without feeling like a major burden.

Refinancing Your Car Loan

Refinancing your car loan involves taking out a new loan to pay off your existing one, often with a lower interest rate or different terms. If your credit score has improved since you first financed the car, or if interest rates have dropped, refinancing could be a viable option. While it won’t erase existing negative equity, a lower interest rate can reduce your overall cost of borrowing, making it easier to pay down the principal and reduce the negative gap over time. It’s important to note that lenders are generally hesitant to refinance loans with significant negative equity.

Other Important Considerations for Negative Car Equity

Beyond direct financial maneuvers, several other aspects can influence your journey out of negative equity. Being mindful of these can help prevent future issues and protect your investment.

- Gap Insurance: This specialized insurance covers the difference between your car’s actual cash value and the amount you still owe on your loan if the car is stolen or totaled. It’s especially valuable when you have negative equity, preventing you from owing money on a car you no longer possess.

- Vehicle Maintenance: Keeping your car in excellent condition helps preserve its resale value. Regular maintenance and prompt repairs can minimize depreciation and make it more appealing to buyers or for trade-in.

- Financial Planning: A comprehensive budget can help you identify areas where you can save money to put towards your car loan, accelerating your path to positive equity.

Comparison of Key Strategies to Address Negative Equity

Understanding the nuances of each option can help you make an informed decision.

| Strategy | Pros | Cons | Ideal Scenario |

|---|---|---|---|

| Selling Outright | Potentially higher sale price than trade-in; complete control over sale. | Requires cash to cover the negative equity gap; time-consuming process. | Have savings to cover the difference; comfortable managing private sale. |

| Trading In & Rolling Over | Convenient, seamless transition to a new car; no upfront cash needed. | Increases new loan amount, higher payments, extended term; pays interest on negative equity. | Need a new car urgently; comfortable with higher payments long-term. |

| Paying Down Faster | Directly reduces principal; builds equity quickly; saves on interest. | Requires consistent extra payments; may not be feasible for all budgets. | Stable income with disposable cash; committed to financial discipline. |

| Refinancing | Potentially lower interest rates; reduced monthly payments. | Difficult to qualify with significant negative equity; doesn’t eliminate negative equity directly. | Improved credit score; interest rates have dropped; minimal negative equity. |

Frequently Asked Questions About Negative Car Finance Equity

What exactly is negative equity in a car loan?

Negative equity occurs when the current market value of your car is less than the remaining balance on your auto loan. You owe more than the vehicle is worth.

Can I sell my car if I have negative equity?

Yes, you can sell your car, but you will be responsible for paying the difference between the sale price and your outstanding loan balance. You must cover this gap to satisfy the lender and transfer the title.

Is it always a bad idea to roll negative equity into a new car loan?

While convenient, rolling negative equity into a new loan is generally not recommended. It increases your total debt, leads to higher monthly payments, and puts you at risk of being upside down on the new loan immediately. It should be a last resort.

How long does it typically take to get out of negative car equity?

The time it takes varies greatly depending on your car’s depreciation rate, your loan terms, and how aggressively you make payments. For some, it might be a year or two; for others, it could be much longer. Making extra principal payments is the fastest way to accelerate the process.

What is gap insurance and how does it relate to negative equity?

Gap insurance (Guaranteed Asset Protection) covers the “gap” between your car’s actual cash value (what your standard auto insurance pays out) and the remaining balance on your loan if your car is totaled or stolen. It’s highly recommended if you have negative equity, as it protects you from having to pay for a car you no longer own.

Navigating negative equity in car finance can feel overwhelming, but it is a solvable problem with careful planning and proactive steps. By understanding your options—whether it’s accelerating payments, exploring refinancing, or strategically handling a sale or trade-in—you can make informed decisions that align with your financial well-being. The key is to avoid ignoring the issue, as it can compound over time and lead to greater financial strain. Taking control of your car loan means taking control of your financial future, ensuring you drive away from debt and towards stability.